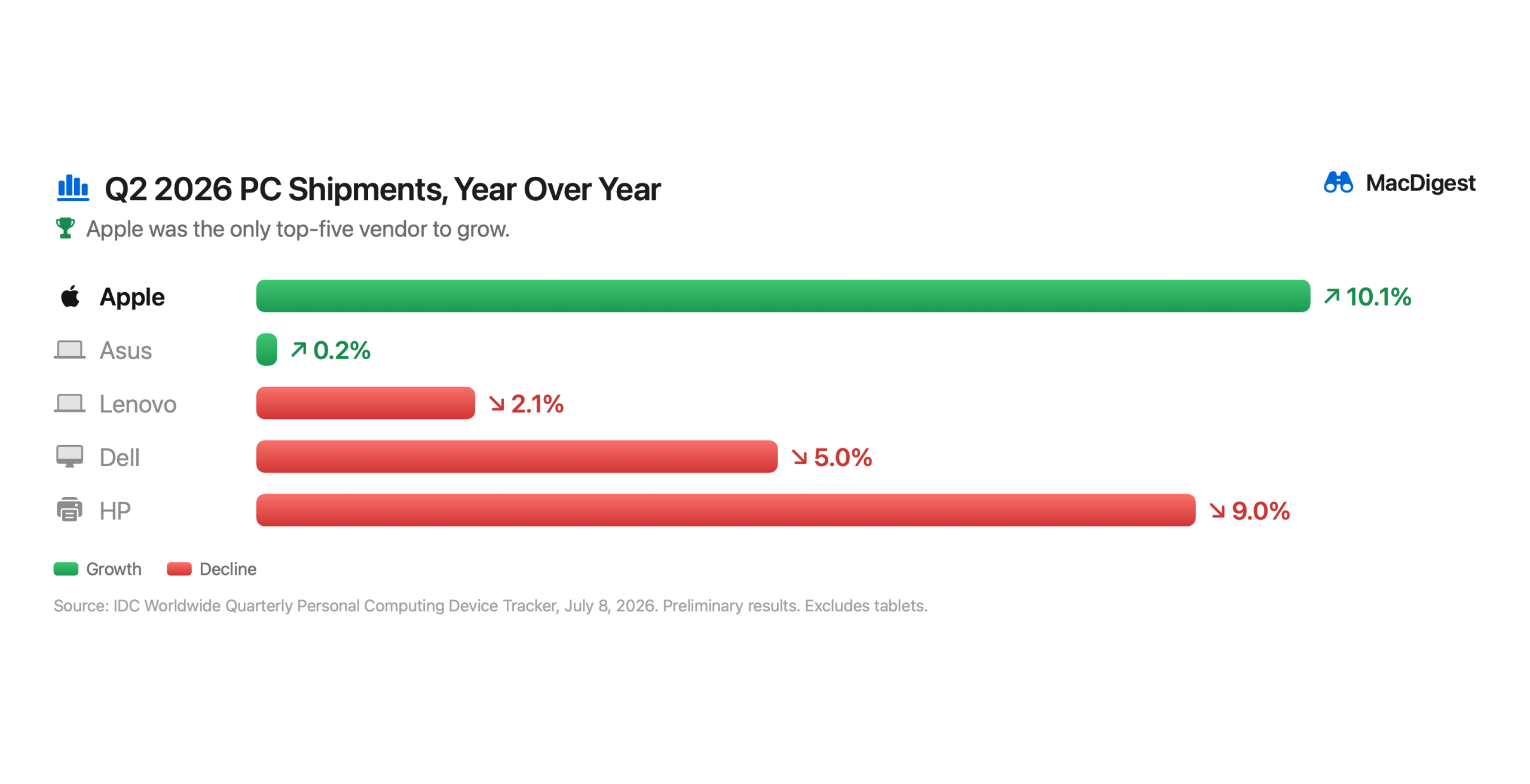

Global PC shipments fell 4.9 percent last quarter to 68.2 million units, the first drop after nine straight quarters of growth. Lenovo, HP, and Dell all shrank. Apple did the opposite, shipping 6.7 million Macs, up 10.1 percent, for 9.9 percent of the market. It was the only top-five vendor to grow.

Apple beats a falling market is the easy story. The better one is why the market is falling, and why the same force dragging everyone down is lifting Apple.

The shortage is not about demand

People didn’t stop wanting PCs. The memory is going elsewhere. Samsung, SK Hynix, and Micron control over 93 percent of DRAM production, and they have shifted capacity to high-bandwidth memory, the kind stacked onto Nvidia and AMD‘s AI chips. A gigabyte of it eats about three times the wafer capacity of the DRAM in a laptop. With Microsoft, Google, Meta, and Amazon spending an estimated $725 billion on data centers this year, the memory makers followed the money.

Consumer memory got squeezed. LPDDR5X, used in thin laptops, jumped 89 percent in a single quarter. DDR4 rose about half. The AI boom is taxing every laptop that isn’t part of it.

Fewer units, more revenue

Shipments are down, but PC revenue is up, because vendors raised prices faster than demand fell. The industry is selling fewer machines for more money. A shrinking market usually signals trouble. This one prints cash for whoever can still get parts.

That last part is the whole story.

Scale decides who wins

In a shortage, supply goes to the biggest buyers. IDC said so twice, through two executives: the largest vendors, with their buying power and supplier ties, are best placed to take share from smaller rivals. Apple ships iPhones, Macs, and servers by the hundreds of millions and buys memory at a scale no mid-size PC maker can match. Smaller brands get tighter supply, higher costs, thinner margins, and IDC expects some to be pushed out.

So the crisis isn’t hitting the industry evenly. It’s concentrating it. The MacBook Neo, Apple’s first sub-$700 laptop, gets credit for the quarter and earned it by reaching buyers Apple never had. But the real story is structural. When memory is scarce, size decides who eats.

IDC expects the rest of 2026 to be worse, with shipments possibly down 20 percent in Q4 and no relief before the end of 2027. A market that harsh rewards the few players big enough to outlast it. Apple is first in line.